Consumer Debt Crisis 2025: The Alarming Rise of Student Loan Delinquencies

It’s always a bit of a mess, isn’t it? Especially when folks start piling up debt. And frankly, what I’m seeing with these student loans… it’s worrying. The New York Fed’s been saying some things, and it seems like a lot of people are struggling. Let’s break it down, shall we?

It’s always a bit of a mess, isn’t it? Especially when folks start piling up debt. And frankly, what I’m seeing with these student loans… it’s worrying. The New York Fed’s been saying some things, and it seems like a lot of people are struggling. Let’s break it down, shall we?

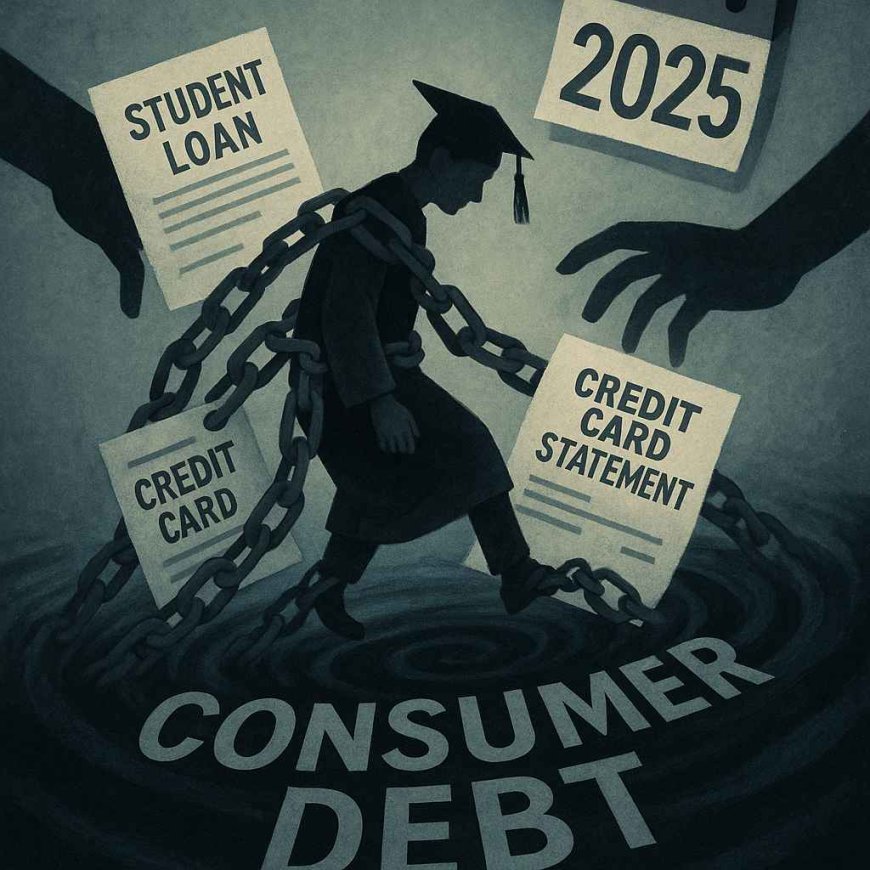

So, the report – and it’s a big one – shows that household debt went up by $167 billion in the first quarter of 2025. That's a jump, alright. It's sitting at $18.2 trillion. And a big chunk of that is coming from student loans. They're reporting a significant increase in seriously delinquent borrowers, which is never a good sign. It’s like a domino effect, you know?

Now, the Fed’s saying that credit card balances are dropping – $29 billion – and auto loans are also down. That’s a bit of a relief, I suppose. Mortgage balances are still climbing, though – $199 billion – which is. well, it’s just more debt. And student loans? They’ve jumped by $16 billion, bringing the total to $1.63 trillion. It’s a massive amount of money, and it's not going away anytime soon.

What’s really concerning is the *way* these loans are going delinquent. The report says they’ve seen a big increase in the rate at which loans are moving from ‘current’ to ‘delinquent’. It's like a wave. And it's mostly due to these past-due student loans that were finally being reported on credit reports after a long pause – a pause that was put in place during the pandemic. It’s like the dam finally broke, and now all that water is rushing through.

They're saying that transition rates into early delinquency held steady for most debts – credit cards, auto loans – but student loans? Boom! A huge spike. It’s a reminder that things aren’t always as simple as the central bank thinks they are. These loans were sitting there, unpaid, for years, and now they're catching up.

What does this *mean* for regular folks? Well, it means that if you've got a student loan, you need to be extra careful. Delinquency doesn’t just mean you’re not paying on time. It can mess with your credit score, making it harder to get a mortgage, a car loan, or even just rent an apartment. It’s a vicious cycle, isn’t it?

And let's be honest, the whole student loan situation has been a mess for years. The government kept extending these payment pauses, and it created a lot of confusion. Now, people are facing a mountain of debt, and they’re struggling to figure out how to pay it off. It's a perfect storm of factors.

The New York Fed is saying that delinquency rates are increasing, but transition into serious delinquency remained stable for auto loans, credit cards, and other debt. It’s a bit of a mixed bag, isn’t it? It's not all doom and gloom, but you need to be aware of the risks.

So, what’s the takeaway here? It’s a reminder that debt is a serious thing. Don't just take on loans without a plan. And if you're struggling to pay them off, don't wait until you're in trouble. Talk to your lender – they might be able to work with you.

Honestly, it’s a bit of a wake-up call, isn’t it? We need to be smarter about how we manage our finances. And the government needs to be more responsible about student loan policies.

Want to learn more? You can find the full report on the New York Fed’s website: https://www.newyorkfed.org/microeconomics/hhdc

What's Your Reaction?